Click on any flag to get an automatic translation from Google Translate. Some news could have an original translation here: News Nouvelles Nieuws Noticias Nachrichten

Mortgage rates for non-residents: Spain’s position in the European landscape

Here is our update of January 2025 with the last available data (November 2024) on Spanish mortgage rates for non-residents from the European Central Bank

One question we receive from our customers nearly daily is: How expensive are the mortgage rates in Spain compared to other European countries?

We were due to do some work on that, and here is the result. At the same time, we took the opportunity to increase our databases, and this article will be updated later. Please note that all charts are interactive, and whenever we update our database, the charts will be updated accordingly.

Thanks to our network of local partners, we offer the best mortgage rates in Spain for those looking to finance a home in Spain. Take 30 seconds to fill out this quick form to get the best Spanish mortgage rates as a non-resident.

-

Mortgage rates in Spain for non-residents: our 2-minute video

Would you like to watch this video in your language? Click on the bottom right of the video on “cc” to get subtitles in your language.

-

While many international buyers prefer to purchase their Spanish second home outright with cash, this approach might not always be the most strategic. Even if you have the means for an all-cash transaction, considering a mortgage could unlock a suite of financial benefits. From diversifying your investments and increasing liquidity to optimising tax efficiencies, the advantages are compelling. Intrigued? We invite you to journey with us through the upcoming sections, where we’ll unveil the nuanced benefits of leveraging a mortgage for your property in Spain—a decision that could redefine your financial strategy.

Securing a mortgage in Spain as a non-resident is a feasible endeavour, though it does come with its unique set of challenges and considerations. Given that the majority of your assets are likely situated outside of Spain, Spanish banks will meticulously evaluate both your financial profile and the property in question to mitigate their risk exposure. Generally speaking, the terms offered to non-residents may be more conservative compared to those available to residents. This often translates to less favourable interest rates, stricter borrowing criteria, and a reduced loan-to-value ratio, meaning you might need to provide a larger down payment. Additionally, the process might involve more comprehensive documentation and a longer evaluation period to thoroughly assess the viability of extending credit under these circumstances. Understanding these nuances and preparing accordingly can smooth the path to acquiring your Spanish property.

-

Comparing Spanish Mortgage rates with European averages

Spanish vs. European Real Estate Financing

Thanks to the detailed database of the European Central Bank that we could import, we were able to run a thorough analysis of mortgage conditions for all European countries compared to Spain. Before examining detailed statistics on various mortgage solutions, we reviewed general conditions for mortgage rates in both Europe and Spain.

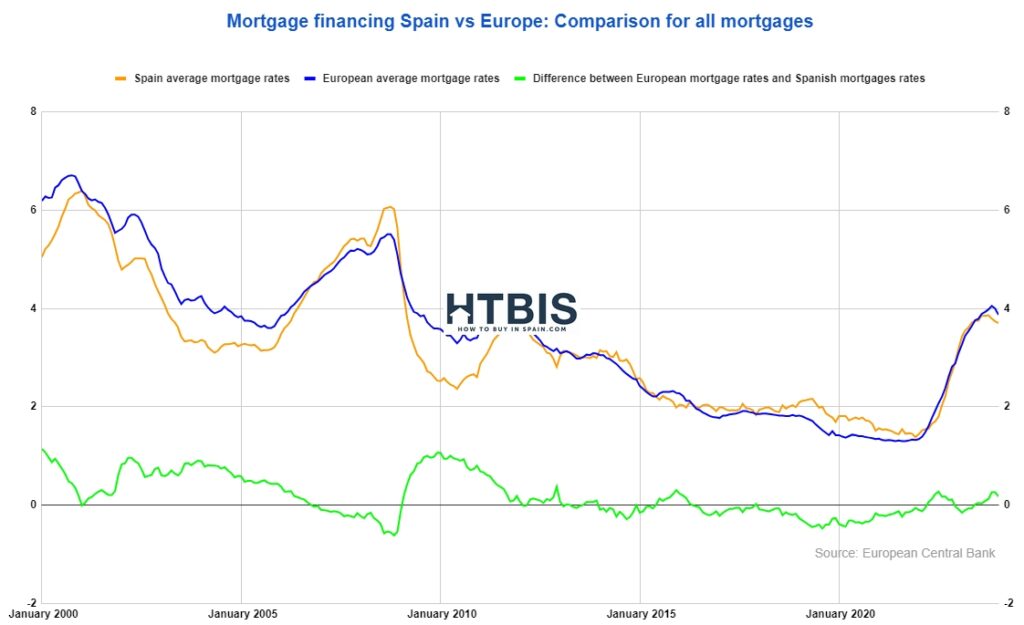

All Mortgages issued in Spain in November 2024 had an average interest rate of 3.04% (vs 3.1% in January 2023) while all mortgages issued in Europe had an average interest rate of 3.44% for the same period (vs 3.19% in Spain in January 2023).The chart below clearly demonstrates a strong correlation between Spanish mortgage rates and their European counterparts. Both datasets, meticulously compiled by the European Central Bank, serve to monitor financial trends across the region. Historically, from November 2014 to April 2022, Spanish mortgage rates consistently exceeded the European average, resulting in a more expensive borrowing climate within Spain. During this timeframe, the average Spanish mortgage rate stood at 2.02%, in contrast to the slightly lower European rate of 1.87%, indicating a notable 0.15% disparity that disadvantaged both the Spanish property market and prospective homeowners.

Spanish mortgage rates are cheaper than European ones

A new trend started in 2022

However, the trend reversed post-April 2022, as Spanish mortgage rates began to align with or dip below the European average. As of November 2024, the most recent data point at the time of this analysis, the average mortgage rate in Spain had settled at 3.04%, marginally below the European average of 3.44%.

This shift represents a significant 0.40% advantage, benefiting both the Spanish real estate market and its investors: Spaniards and foreigners, and reflects a notable improvement in the affordability and attractiveness of Spanish mortgages relative to the broader European landscape.

Now that we have analysed all the mortgages issued in both Europe and Spain, it is time to compare rates for different mortgage solutions. As you know, mortgage rates are separated into two big categories:

- fixed-rate mortgages, mostly mortgages that will keep the same rate over the full mortgage length, usually between 10 and 25 years,

- Variable-rate mortgages, mortgages that will change rates over the life of the mortgage (monthly, yearly, or every five years)

In the following analysis, we will delve further into the nuances of four distinct mortgage categories: variable-rate mortgages, fixed-rate mortgages with terms of 1-5 years, those with terms of 5-10 years, and fixed-rate mortgages with a term of 10 years. Notably, variable-rate and 10-year fixed-rate mortgages stand out as the most popular choices among individuals financing their home purchases, both across Europe and specifically within Spain. This comparison aims to illuminate the characteristics and trends that define each category, providing a comprehensive overview of the Spanish mortgage landscape.

Here are all the evolutions and a quick analysis for each:

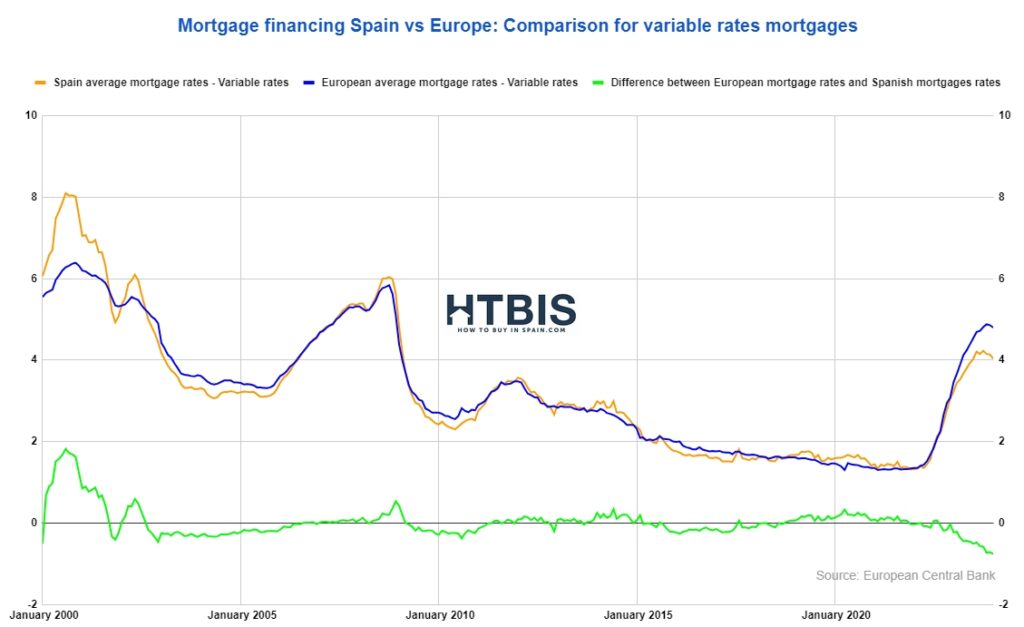

Variable Mortgage rates: Spain vs Europe showdown

As you can see on the chart, Spanish mortgage rates since April 2022 were nearly always cheaper than mortgages in Europe, and as of November 2024, they are more affordable by 0.40%.

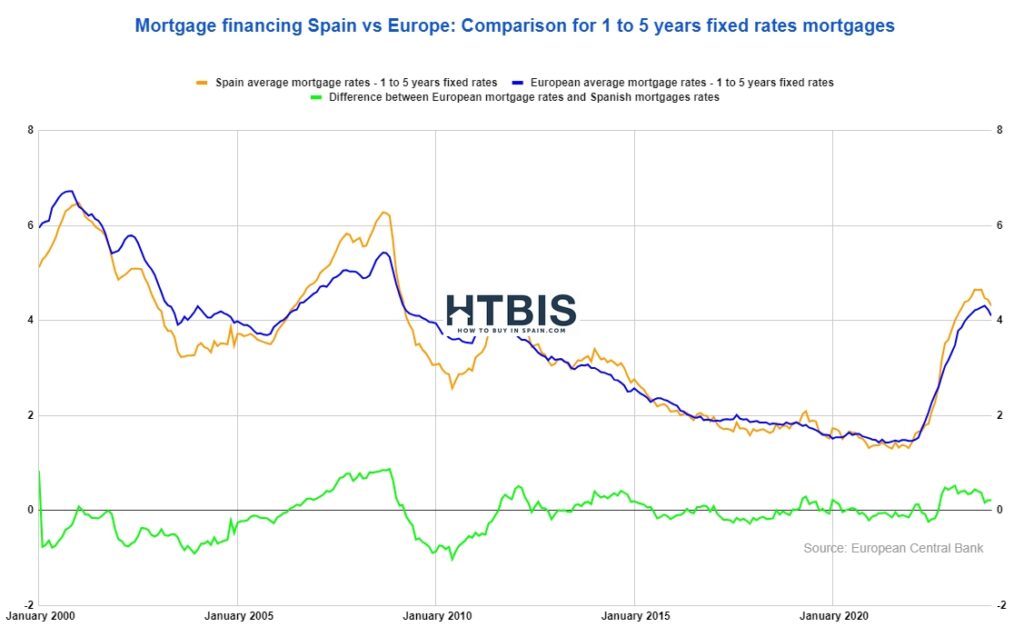

1-5 years fixed Mortgage rates face-off: Spain vs Europe

As you can see on the chart, Spanish mortgage rates with fixed rates between 1 and 5 years are one of the only Spanish mortgage rates for which you will pay more than in other European countries. On average, as of November 2024, you will pay 0.21% more.

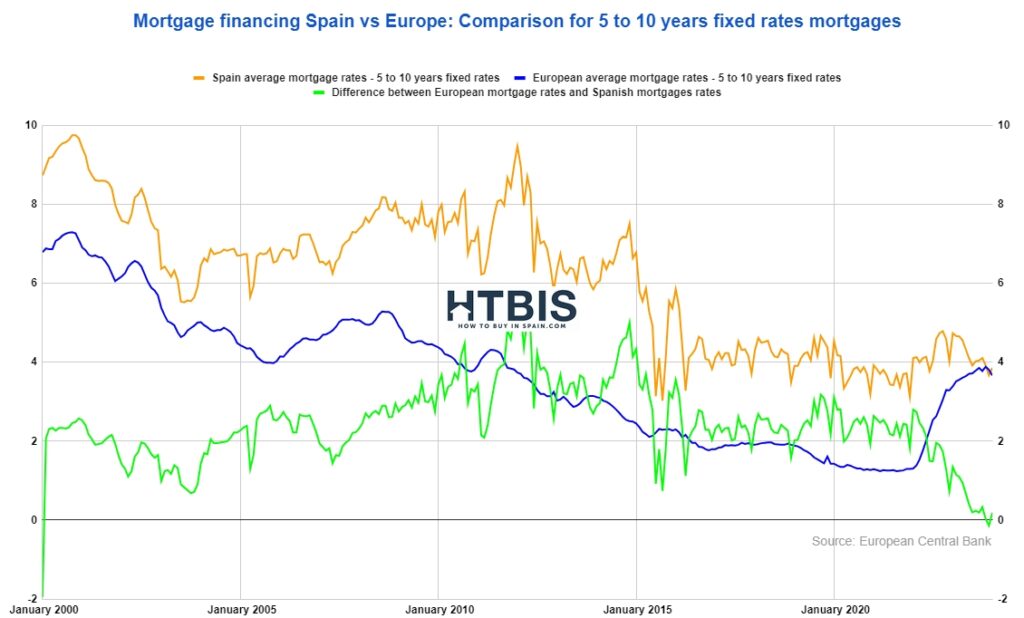

5-10 years fixed Mortgage Rates: Spain vs Europe head-to-head

As you can see on the chart, fixed Spanish mortgage rates (ranging from 5 to 10 years) were consistently more expensive in Spain than in other European countries. Interestingly, as of November 2024, Spanish mortgage rates trade close to the European average, i.e. no more premium than in the past.

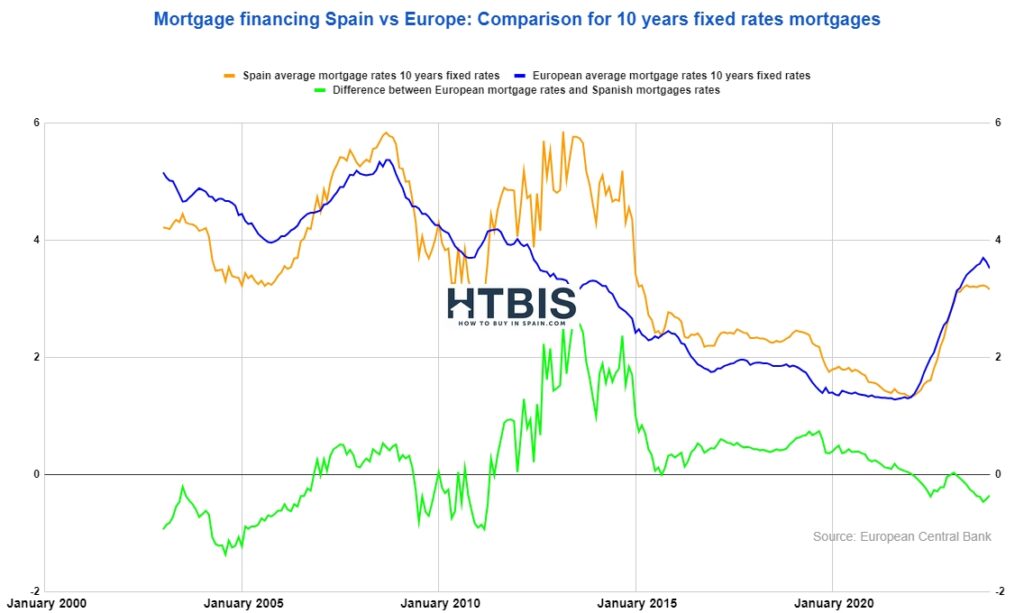

10-Year fixed Mortgage rates in Spain versus Europe

As you can see on the chart, Spanish mortgage rates since March 2022 are cheaper than mortgages in other European countries, as of November 2024, they are cheaper by 0.36%. This is excellent news for real estate buyers in Spain.

Read more on the subject: What are the best Spanish mortgage rates?

-

Key factors behind the advantageous Spanish Mortgage rates

Thanks to our detailed update, now you know that the Spanish mortgage market is experiencing a confluence of positive factors that set it apart from other European counterparts:

- Spanish property values remain attractively priced when compared to other European real estate markets, presenting a compelling value proposition and a lower risk for lending banks, unlike the situation in 2008.

- The Spanish economy exhibits resilience and robustness, outpacing the broader European economic performance, which instils confidence in both domestic and international investors.

- The impact of energy price fluctuations has been mitigated effectively in Spain since the escalation of geopolitical tensions in Ukraine, contributing to a more stable cost of living and operating environment.

- Spain’s inflation has consistently been lower than the European average, preserving purchasing power and contributing to the overall economic stability.

- The Spanish real estate sector is characterised by its prudence and lack of speculative excess, evident in the modest percentage of transactions involving mortgages (66%) and the conservative loan-to-value ratio, which averages 60%. This reflects a healthy level of leverage and risk appetite in the market.

- The strength of the general economy in Spain suggests that Spanish banks are in a sound financial position, enabling them to offer attractive financing options without resorting to aggressive lending practices. This economic stability is likely to support continued favourable mortgage rates.

These elements collectively create a conducive environment for the advantageous spread in Spanish mortgage rates, underscoring the market’s resilience and appeal to a broad spectrum of investors. Additionally, the prudent regulatory framework and proactive fiscal policies may further bolster the market’s attractiveness, potentially leading to sustained growth and stability in the Spanish real estate sector.

Why Spanish mortgage rates are less expensive than in other European countries?

-

What are the advantages of obtaining a Mortgage in Spain as a non-resident?

Increase the return on your Spanish property investment

The main advantage of buying a property in Spain is that current real estate levels are not crazy if you compare those to other European countries.

Read more on the subject: What return will you make on your Spanish property?Even with current mortgage rates, getting a mortgage is easier than getting a loan for something else as a person as the bank has the property as collateral. So, while we always encourage our customers to manage risks and don’t overleverage, getting a mortgage before buying a property is in our mind a wise way to diversify your financial assets.

Last but not least, depending on your home country, real estate assets could be less taxed than other financial assets.Diversify your investments

By taking a mortgage, you can decrease your risks by keeping some funds for other investments.

Potential tax benefits and how to maximise them

Buying a property with a mortgage can provide significant tax benefits if you subsequently put the property on the rental market as a “buy-to-let” or investment property. Please consult our tax advisors for more information on that.

Advantages of Spanish mortgage rates for UK residents

In the mortgage landscape, UK banks are known to promote variable-rate mortgages, nudging customers towards options that fluctuate with the market, despite the inherent uncertainty in future repayments. Meanwhile, Spanish banks are more accommodating of fixed-rate mortgages, offering borrowers the chance to lock in a stable and predictable payment schedule throughout the loan term, contrasting with the UK’s bank-driven preference for variable rates.

Spanish mortgage rates for US residents

In the US mortgage market, fixed-rate mortgages are predominant, offering long-term stability with terms commonly set at 30 years, allowing homeowners to lock in rates for the duration of their loan. This contrasts with the Spanish market, where, despite a growing preference for fixed-rate options, mortgages typically have shorter terms and the market historically leaned more towards variable rates, influenced by the Euribor. Additionally, the US market is characterised by its diversity in loan products and a more developed secondary market for mortgages, which enhances liquidity and flexibility in terms and conditions. In contrast, Spain’s market is more traditional and less varied in its offerings.

Benefits for a non-resident of financing his property in Spain with a mortgage.

-

How to get the best mortgage rate as a non-resident in Spain?

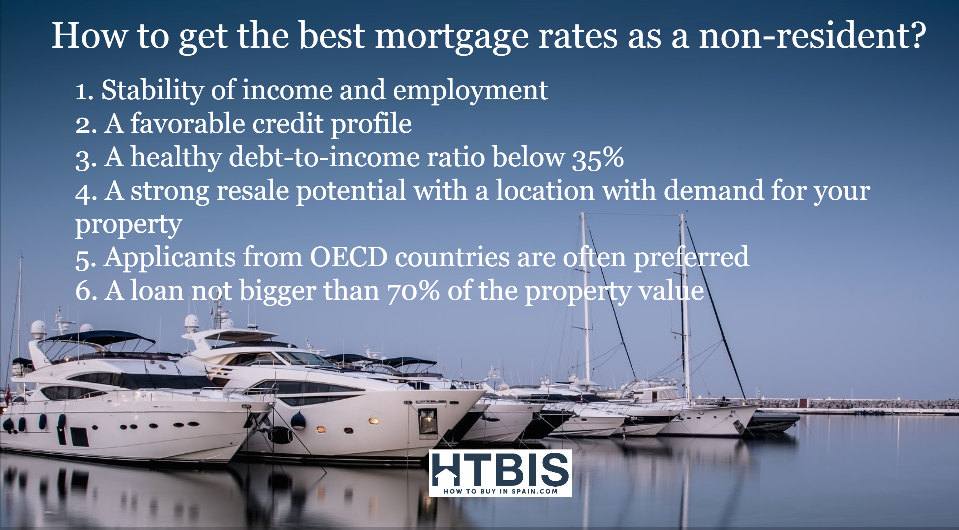

Have the best customer profile for the Spanish bank

Here are some insights into what constitutes an attractive customer profile for securing a mortgage:

- Employment and stability: Ideal candidates are employed with a stable and substantial income.

- Creditworthiness: A favourable credit history with minimal debts relative to income is crucial.

- Debt management: A healthy debt-to-income ratio below 35. This means that monthly net income would be at least three times greater than debt repayments.

- Property value: 1/ The chosen property should hold strong resale potential. 2/It should be priced appropriately within the current market. 3/It should be in a location with consistent demand.

- Geographic consideration: Applicants from OECD countries are often preferred due to stringent anti-money laundering regulations across Europe. Being an EU resident further simplifies the process.

- Maximum loan amounts for non-residents: Spanish banks would like to keep that under control

Avoid taking a mortgage that is too large compared to the property’s value.

As a non-resident, you’re eligible to secure a mortgage for your second home or investment property. Since your assets are not located in Spain, banks will typically require guarantees and generally cap the loan-to-value (LTV) ratio at 70%. The LTV ratio represents the portion of the property’s pre-tax value that can be financed through a mortgage. This percentage serves as a general guideline. Feel free to request a complimentary consultation from our mortgage broker, who is well-versed in the process and familiar with Spanish banks that are favourable towards foreign clients. The lower this ratio is, the lower the risk for the bank and the better rate for your mortgage.

How to get the best rates as a non-resident.

-

Practical considerations for your Spanish mortgage as a non-resident

Processing time for Mortgage applications

On average, mortgages are processed quickly, but keep in mind that you need to prepare a full file so the bank can establish your credit profile. Our partner will work with you on that. Don’t worry.

Higher interest rates and reduced loan amounts for non-residents

Generally, foreigners will receive slightly less favourable conditions for their mortgages than Spaniards. This is normal as foreigners don’t have all their financial assets and incomes based in Spain. With a good credit profile and a reasonable loan-to-value ratio, our customers receive competitive quotes.

NIE number for non-residents

Obtaining an NIE number is a crucial step for non-residents seeking to navigate the property and mortgage landscape in Spain. This identifier serves as your tax identification number. It is essential for various legal and financial transactions, including the purchase of property and the application for a mortgage. Fortunately, obtaining an NIE is a straightforward process. Your legal representative can handle it on your behalf if time constraints are an issue. For a detailed guide on acquiring your NIE and its importance, we invite you to explore our comprehensive article: Your Spanish NIE number and how to obtain it.

Useful considerations for a non-resident to get a Spanish mortgage

-

Comparing Mortgage rates in Spain vs. selected European countries

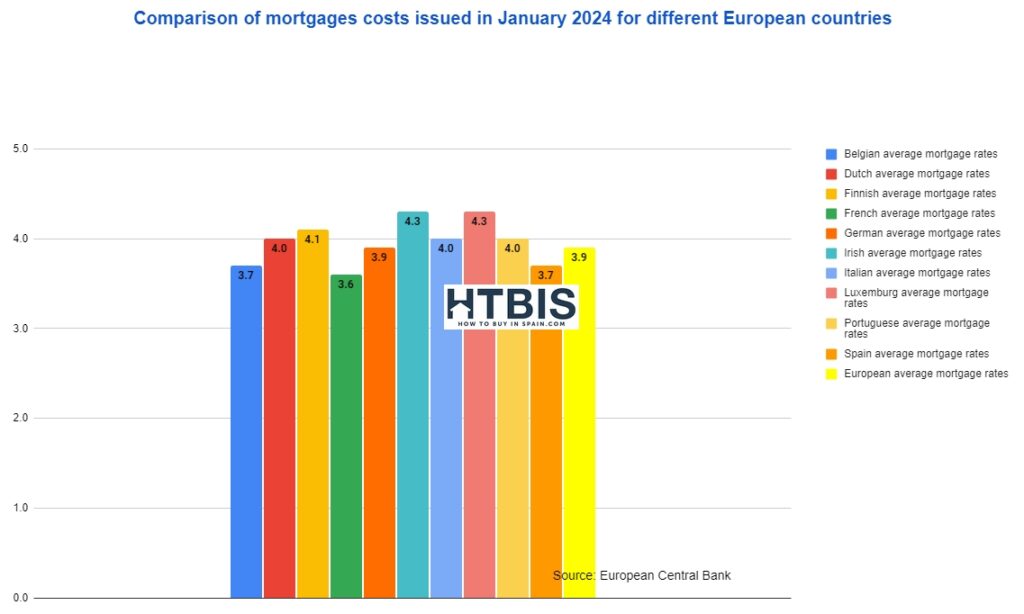

Before examining the evolution of mortgage conditions between Spain and a few countries, let’s take a look at the current situation as of November 2024. Here is the evolution of the different European markets, sorted alphabetically. As a reminder, Spanish mortgage rates and European mortgage rates were at 3.04% and 3.44%, respectively, as of the end of November 2024.

European mortgage rates November 2024 leaderboard

- Belgian mortgage rates are issued with a 3.19% rate on average in November 2024

- Dutch mortgage rates are issued with a 3.71% rate on average in November 2024

- Finnish mortgage rates are issued with a 3.31% rate on average in November 2024

- French mortgage rates are issued with a 3.17% rate on average in November 2024

- German mortgage rates are issued with a 3.59% rate on average in November 2024

- Irish mortgage rates are issued with a 3.94% rate on average in November 2024

- Italian mortgage rates are issued with a 3.69% rate on average in November 2024

- Luxembourg’s mortgage rates are issued with a 3.29% rate on average in November 2024

- Portuguese mortgage rates are issued with a 3.04% rate on average in November 2024

Here is the same information presented in a column chart:

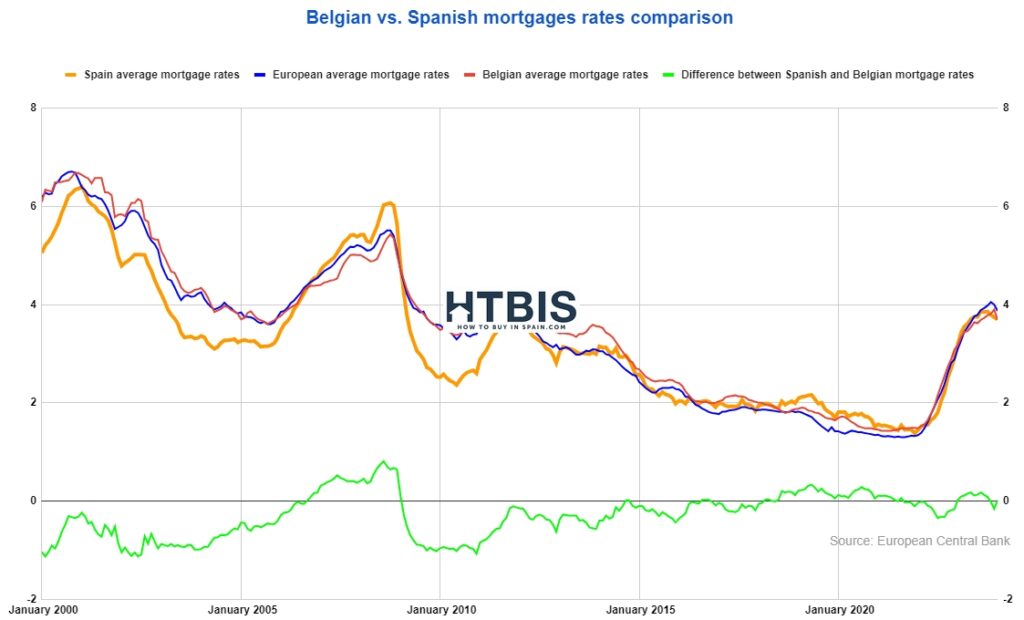

Belgian mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Spanish mortgage rates and Belgian mortgage rates are close to each other in November 2024. As of November 2024, Belgian mortgage rates were issued at 3.19%, 0.15% higher than Spanish mortgages.

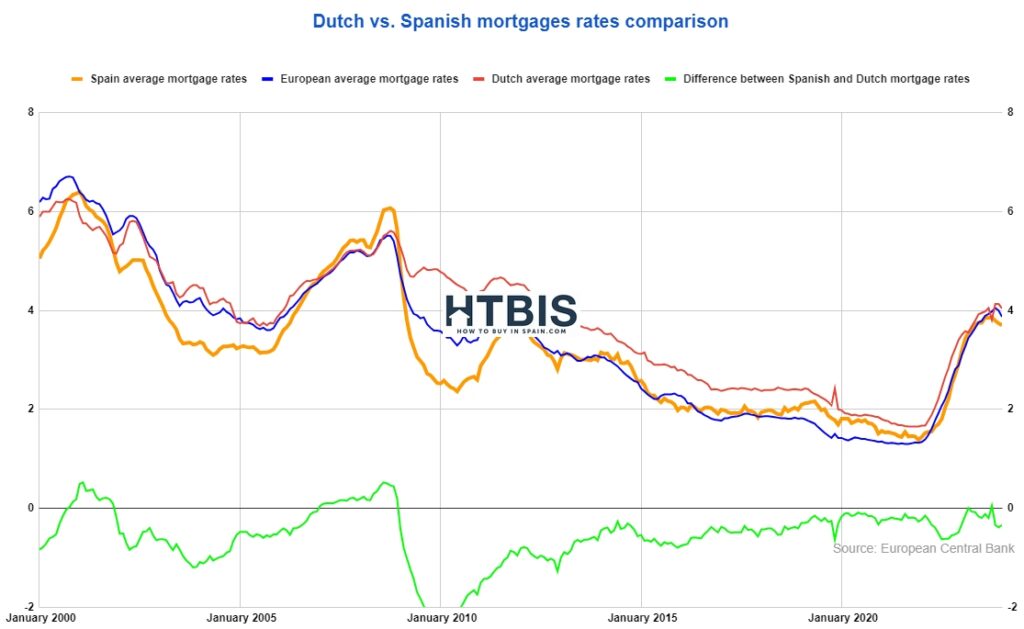

Dutch mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Spanish mortgage rates are more expensive than Dutch mortgages by 0.67%. In November 2024, Dutch mortgage rates were sold at 3.71%.

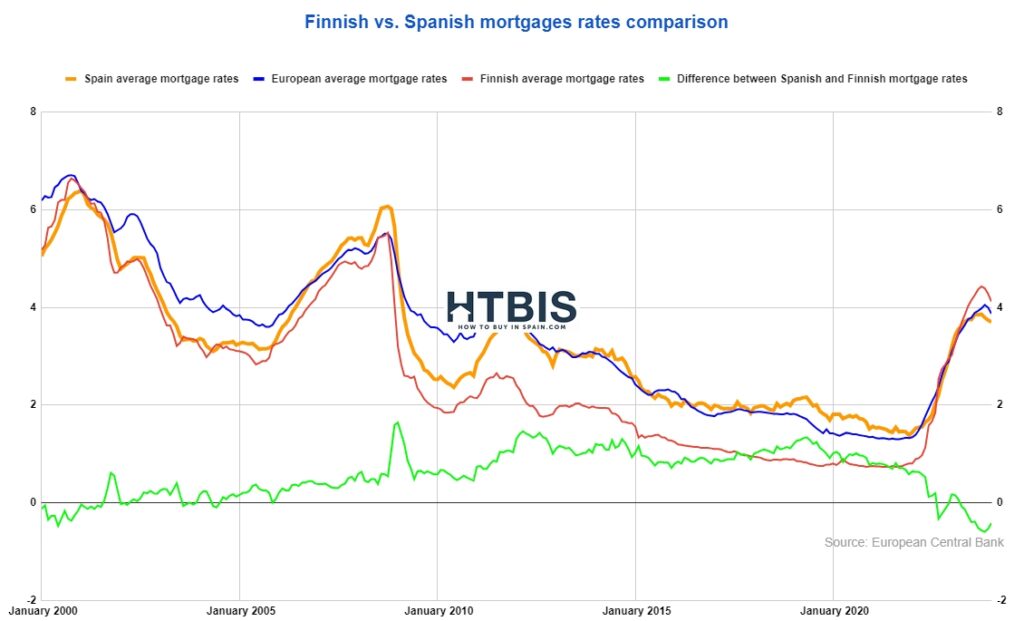

Finnish mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Spanish mortgage rates since March 2022 have been cheaper than those in Finland, and as of November 2024, they are 0.27% more affordable. This is excellent news for real estate buyers in Spain. In November 2024, the Finnish mortgage rate was set at 3.31%.

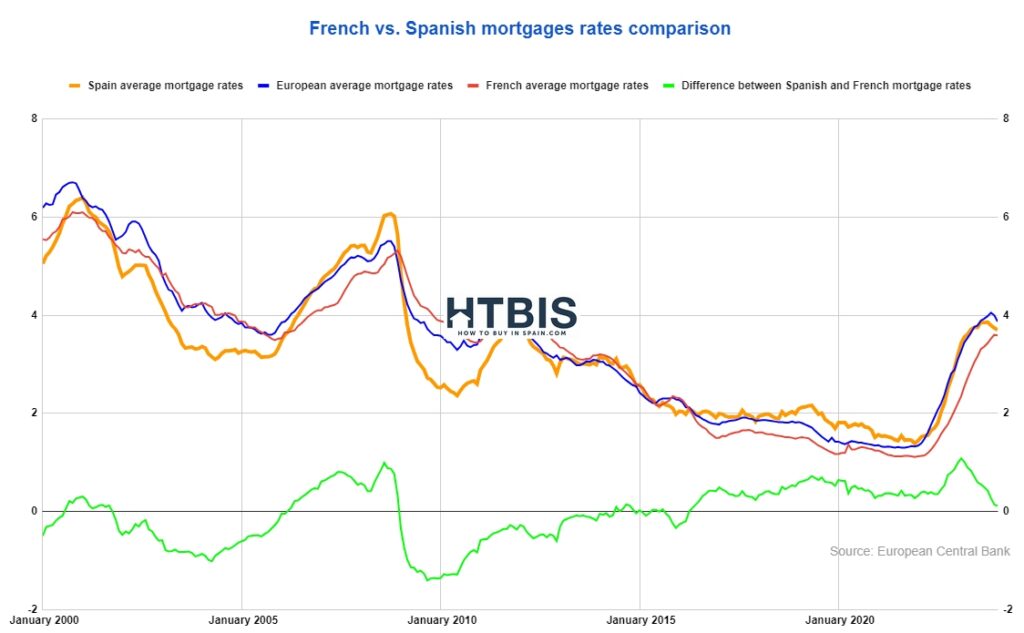

French mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, French mortgages are little bit more expensive than Spanish mortgage rates in November 2024. They trade at 3.17%

German mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As shown on the chart, as of November 2024, Spanish mortgage rates are 0.55% lower than German mortgage rates. This is excellent news for real estate buyers in Spain. In November 2024, German mortgage rates were sold at 3.59%.

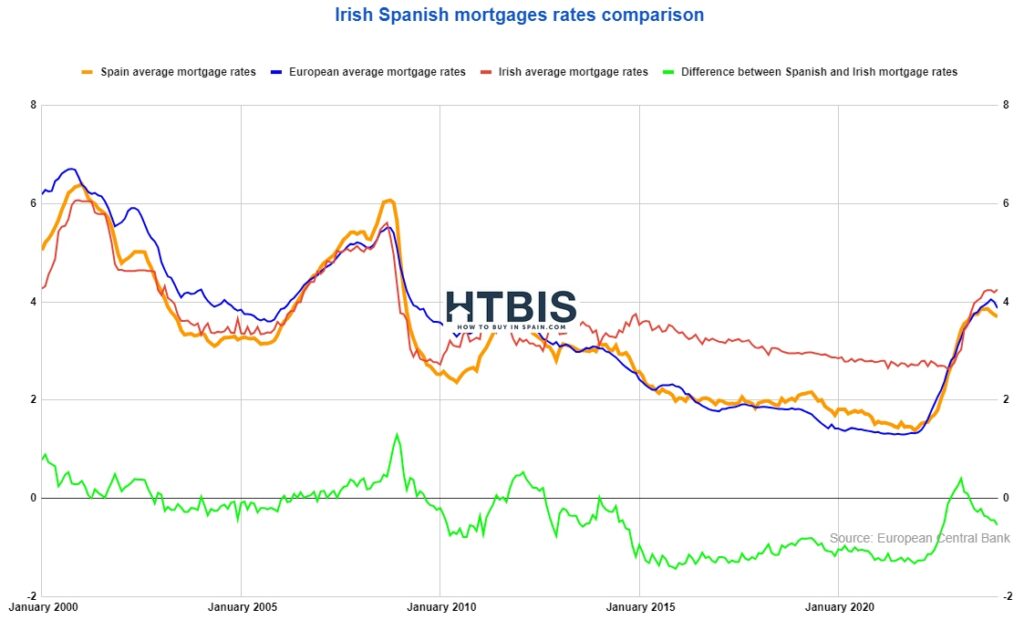

Irish mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Irish mortgages are much more expensive than Spanish mortgages. As you will surely know, the Irish real estate market rebounded strongly and is one of the hottest markets in Europe, even with those higher rates. In November 2024, Irish mortgage rates were trading at 3.94%, 0.9% higher than Spanish mortgage rates.

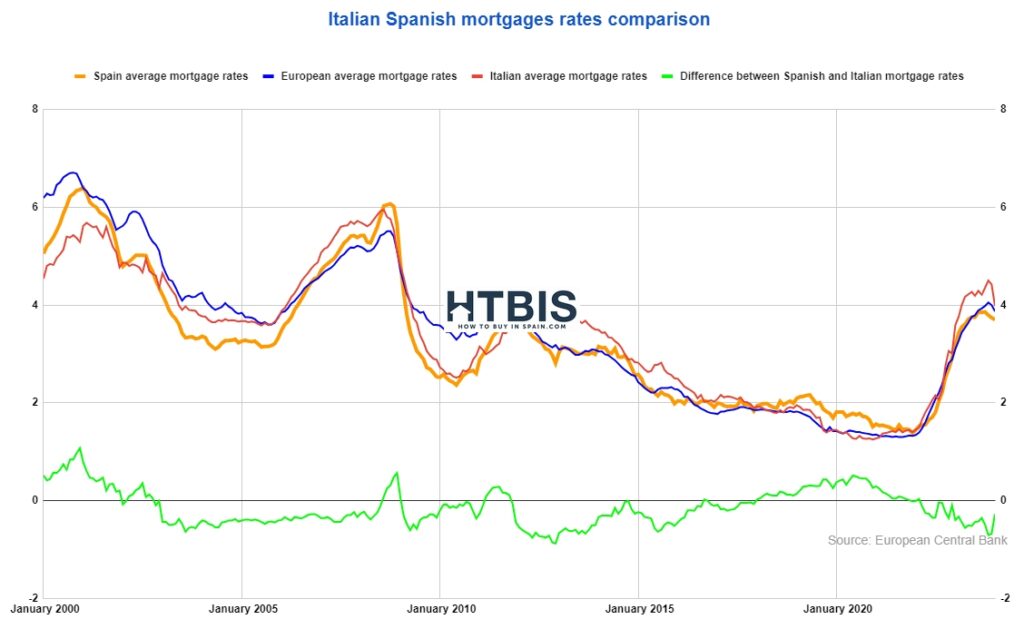

Italian mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Italian mortgages are much more expensive than Spanish mortgages. In November 2024, Italian mortgage rates were trading at 3.23%, 0.19% higher than Spanish mortgage rates.

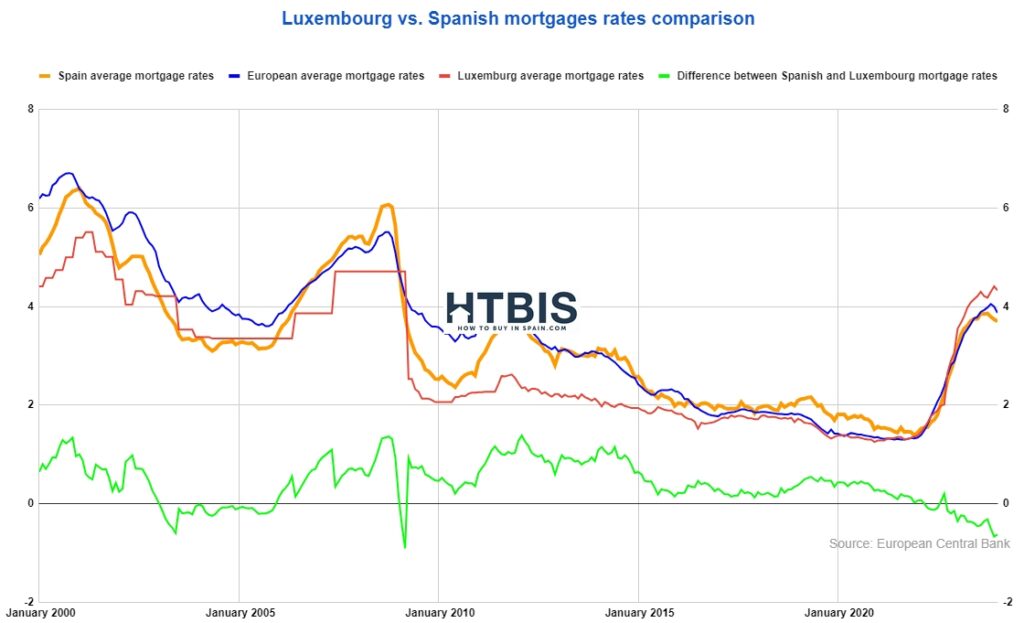

Luxembourg mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Luxembourg mortgages are much more expensive than Spanish mortgages. In November 2024, Italian mortgage rates were trading at 3.69%, 0.65% higher than Spanish mortgage rates. As you probably know, the Luxembourg real estate market has a very high valuation, and we could see this as banks being prudent or instructed by the European Central Bank to be cautious.

Portuguese mortgage rates vs. Spanish mortgage rates evolution over the last 20 years

As you can see on the chart, Portuguese mortgages are much more expensive than Spanish mortgages. In November 2024, Portuguese mortgage rates were trading at 3.29%, 0.25% higher than Spanish mortgage rates. The Portuguese real estate market had a nice run, too, and we could see some caution from Portuguese banks.

-

Further readings

- Read more on current financing conditions in Spain with our detailed article: What are the best Spanish mortgage rates?

- Hesitating between fixed or variable rates on your mortgage (in Spain or elsewhere) have a look at our detailed insights: How do I choose between fixed and variable rates for a mortgage?

- Last but not least don’t miss our detailed ultimate guide to your Spanish mortgage

- If you need a mortgage pricer for your Spanish mortgage, check our article for more.

Stéphane

Senior analyst and strategist at HTBIS

Stéphane, with over 20 years of experience in real estate, finance and entrepreneurship, is the co-founder of www.howtobuyinspain.com. With an extensive network of local partners in Spain, his deep commitment to the real estate sector, combined with strong analytical skills and a problem-solving mentality, has fueled his success. Constantly eager to learn and passionate about teaching, Stéphane believes in the power of knowledge sharing to master any subject.

Spanish Mortgage Rates for Non-Residents FAQ

Are Spanish mortgage rates cheaper than other European countries?

Yes, as of November 2024, Spanish mortgage rates average 3.04% compared to the European average of 3.44%. Spain offers a 0.40% advantage, making it more affordable than most European markets including Germany, Italy, and Ireland.

Can non-residents get mortgages in Spain?

Yes, non-residents can secure Spanish mortgages with up to 70% loan-to-value ratio. Banks typically require a stable income, a good credit history, and comprehensive documentation. The process takes longer than for residents but offers competitive rates.

What are the main benefits of getting a Spanish mortgage as a non-resident?

Key benefits include diversifying investments, increasing liquidity, potential tax advantages for rental properties, leveraging competitive rates below European average, and accessing Spain's stable property market with conservative lending practices.

How can non-residents get the best Spanish mortgage rates?

Maintain stable employment, excellent credit history, keep debt-to-income ratio below 35%, choose properties with strong resale potential, and work with experienced mortgage brokers who specialize in non-resident financing.

How long does the Spanish mortgage application process take for non-residents?

Spanish mortgage applications typically process within 3-6 weeks for non-residents. The timeline depends on documentation completeness, property valuation, and bank approval procedures. Proper preparation accelerates the process significantly.

What is the maximum loan-to-value ratio for non-residents in Spain?

Non-residents can typically finance up to 70% of the property value in Spain. This means a minimum 30% down payment is required. Lower ratios may secure better interest rates.

Why are Spanish mortgage rates more competitive than other European countries?

Spain benefits from robust economic performance, controlled inflation, stable property values, conservative lending practices with 60% average LTV, and strong banking sector health, creating favorable borrowing conditions.

How do Spanish mortgage rates compare to France and Germany?

As of November 2024, Spanish rates (3.04%) are lower than German rates (3.59%) and competitive with French rates (3.17%). Spain offers better value than most major European markets.

What documents do non-residents need for a Spanish mortgage application?

Required documents include NIE number, income statements, tax returns, bank statements, employment contract, credit report from home country, and property valuation. Professional guidance ensures complete documentation.

Are fixed or variable mortgage rates better in Spain for non-residents?

Spanish banks accommodate both options. Fixed rates provide payment stability and predictability, while variable rates may offer initial savings. Current market favors fixed rates for long-term security.

Downloadable Charts